This piece engages with "Europe's defence startups face even bigger hurdles than America's," published in The Economist on April 23, 2026. We add European numbers, name the reform models that are already working, and argue why this question matters for the Vienna conversation on May 19.

The Argument, Restated

The Economist's framing, captured in the magazine's own promotion of the piece, is direct: "Europe will need many more entrepreneurs willing to take big risks if it is to reinvigorate its defence industry and reduce its reliance on American arms." The implication is sharper than it sounds. It is not enough for Europe to spend more on defence. It must also rewire the path through which defence money reaches the companies actually capable of moving fast — and that rewiring is structurally harder in Europe than it is in the United States.

The American story is now familiar. A small group of venture-backed disruptors, the so-called neoprimes — Anduril, Palantir, Shield AI, and a handful of others — have built government revenue at a CAGR roughly four times that of the legacy primes between 2020 and 2024 (Archyde, citing S&P Global Market Intelligence). They moved fast because the procurement system, however imperfectly, learned to let them. Open-topic SBIR contracts, multiple-award IDIQ frameworks, and the Defense Innovation Unit's Commercial Solutions Opening mechanism made it possible for a young company to win a meaningful first contract without first becoming a prime sub-supplier.

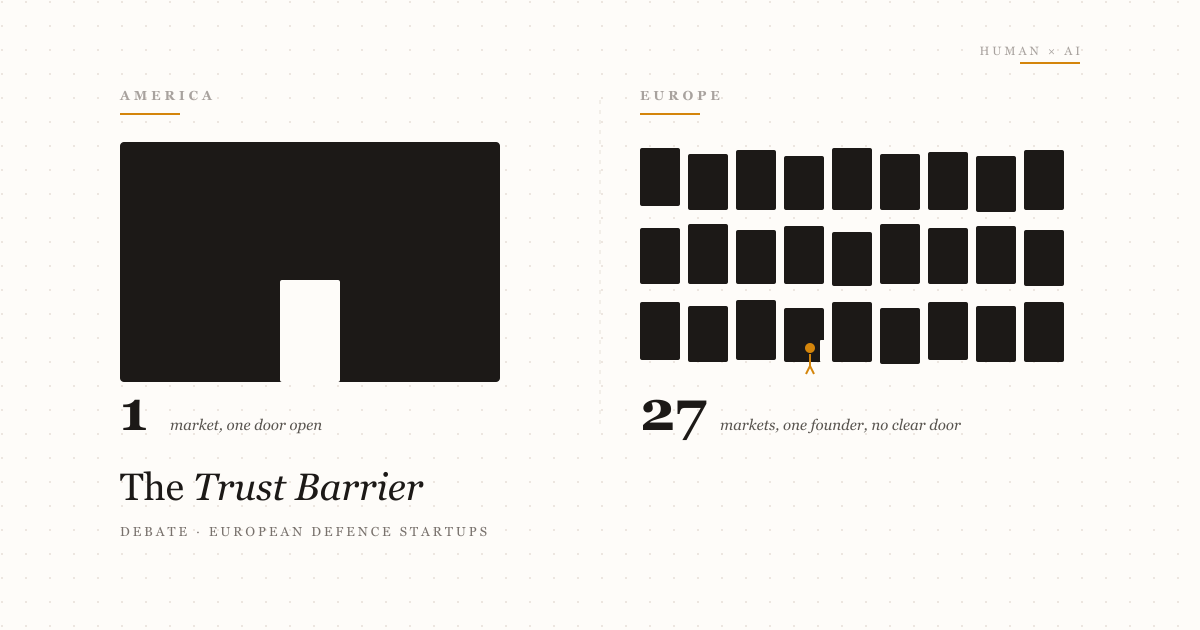

The European story is structurally different. The wall is not built of any one bad rule. It is built of twenty-seven of them.

The Fragmentation Tax

The single most consequential number in the European defence procurement debate comes from Bruegel's April 2026 policy brief on European defence procurement: in Germany, Poland, and the United Kingdom, the top-ten contractors capture between 67% and 90% of national procurement spending. In the United States, the equivalent share is under 40%. The American defence-industrial base is concentrated; the European one is concentrated and fragmented across national borders, which leaves the bottom of the market — where startups live — squeezed twice.

The second number is even more telling. According to the same Bruegel analysis, the United States has roughly 469 more defence-tech startups than the EU, the United Kingdom, and Ukraine combined. That is not a measurement of culture or appetite for risk. It is a measurement of how many doors the system actually opens. Until 2024, only two startups appeared in the procurement records of Germany, Poland, and the UK over the entire period studied. Two.

The third number is procurement velocity. Germany's K130 corvette, commissioned in the early 2010s, is sixteen years old and still cannot deploy drones. Ukraine, by reforming its approval process, has compressed the time from prototype to deployed system from one to two years down to two weeks. The gap is not incremental. It is a category difference.

Why "Just Spend More" Will Not Be Enough

Europe is now spending more. NATO defence budgets are rising; Germany's defence spending alone is projected to climb from €86 billion in 2025 to €152 billion by 2029. The NATO Innovation Fund has committed over €1 billion to deep-tech and dual-use startups. Major contracts have begun to land at venture-backed companies: Helsing's €300 million drone contract, Quantum Systems' €210 million order, Stark's €300 million deal, all in 2025 (Bruegel, 2026).

This is real progress. It is also, as The Economist argues, not yet enough — because money alone does not create the conditions for a self-sustaining startup defence-tech ecosystem. What money does is reveal which parts of the procurement architecture are still load-bearing for incumbents. When new euros enter a system designed to flow toward primes, they flow toward primes. The reforms that matter are the ones that change the path of the money, not just its volume.

The Reform Models That Already Work

The good news embedded in The Economist's argument is that the reform playbook is not theoretical. It is being executed in three places — and Europe has line-of-sight to all of them.

Ukraine has built, under the pressure of war, the most aggressive defence-startup pipeline on the continent. The Brave1 platform has issued more than 540 grants to over 1,500 participating companies, with a total disbursement of around $50 million and individual awards scaled by readiness from $11,000 to $186,000 (Bruegel, 2026). Crucially, Ukraine also runs a digital marketplace, Brave1 Market, allowing army units to purchase directly from manufacturers. The procurement loop is closed in days.

Israel has formalised a similar pathway through the DDR&D programmes — Green Lane, Innotal, InnoFense, and Meimad — that allow startups to enter the system via simplified contracts, retained IP, and time-boxed feasibility funding. Between October 2023 and September 2024, Israel directed $189 million to 86 startups and small companies. Startup orders increased fivefold over a single year.

France, through the Agence de l'Innovation de Défense, has lifted the SME share of defence spending from 14% to 25% in two years — a faster reform of national procurement than any other large European country has yet achieved. In February 2026, France launched a joint programme with Ukraine for competitive grants and direct battlefield testing.

None of these models requires Europe to invent new mechanisms. They require Europe to adopt mechanisms that already exist, and to harmonise them across borders so that a Munich-based defence-tech founder can sell to Warsaw, Stockholm, and Lisbon without rebuilding a compliance stack at every border.

Why This Belongs in the Vienna Conversation

Defence-tech is the cleanest test case for whether Europe can act as a single technology market. The geopolitical pressure is undeniable. The capital is, for the first time in decades, available. The startups exist — Helsing, Tekever, Quantum Systems, ARX Robotics, ICEYE, Stark, Donaustahl, and dozens of less visible companies are already deploying systems in the field. What is missing is the procurement architecture that lets these companies scale on continental terms rather than national ones.

This is not a defence question alone. It is the same question that every European AI founder, quantum founder, and dual-use founder is asking in a different vocabulary: can the continent's twenty-seven separate buyers behave, when it matters, like one buyer? The Economist's piece reframes that question through the most demanding lens available — defence — and concludes that the hurdles are bigger here than they are across the Atlantic. The numbers support the framing.

The follow-on question is operational: which of the reform models above does Europe pick up first, and at what level — national, EU, or NATO? That is the kind of question a room of founders, investors, and policymakers in Vienna on May 19 is built to answer. The Sovereign Capital panel with Joachim Enegaard, Tichomir Jenkut, Jeremy Teboul, and Valentin Tabus, moderated by Valeri Petrov, sits exactly on this fault line.

Implications

- For policymakers: The bottleneck is not the absence of capital but the architecture of procurement. Europe's twenty-seven national systems impose a tax that compounds at every cross-border sale. The single most leveraged reform is mandatory multiple-award framework contracts, modelled on US IDIQs, opened deliberately to non-prime suppliers.

- For founders: The countries that have moved fastest — France, Ukraine, Israel — are the countries where you can today win a first defence contract on a startup timeline. Wait for harmonisation at your peril; build into the reformed national entry points first, harmonise the legal stack second.

- For investors: The neoprime category exists in Europe in nascent form. Helsing, Quantum Systems, Tekever, and Stark are early proof. The bet that Europe replicates the US neoprime trajectory is no longer contrarian; the bet that it does so at scale within five years still is.

Frequently Asked Questions

Q: What is the central argument of The Economist's April 23, 2026 piece on European defence startups?

A: The Economist argues that Europe's defence startups face even bigger structural hurdles than American ones — fragmented national procurement systems, lengthy approval cycles, and risk-averse funding mechanisms that favour incumbents — and that Europe will need many more entrepreneurs willing to take big risks if it is to reinvigorate its defence industry and reduce its reliance on American arms.

Q: What are "neoprimes" and why do they matter?

A: "Neoprime" is the label for venture-backed defence-tech disruptors — most prominently Anduril and Palantir in the United States — that operate with software-first architectures and deliver capability faster and leaner than legacy prime contractors. Their government-revenue growth between 2020 and 2024 has been roughly four times that of legacy primes. Europe is producing early-stage equivalents (Helsing, Quantum Systems, Tekever, Stark, ARX Robotics) but at a much smaller scale.

Q: How concentrated is European defence procurement compared to the United States?

A: According to Bruegel's April 2026 analysis, the top-ten contractors in Germany, Poland, and the United Kingdom capture between 67% and 90% of national defence procurement spending. The equivalent figure in the United States is below 40%. Europe is more concentrated and, because it is fragmented across 27 national systems, harder for new entrants to crack.

Q: Which European countries are reforming defence procurement fastest?

A: France lifted the SME share of defence spending from 14% to 25% in two years through the Agence de l'Innovation de Défense. Ukraine reduced deployment time from one to two years to as little as two weeks via the Brave1 platform and Brave1 Market. Israel has built dedicated startup-entry programmes (Green Lane, Innotal, InnoFense, Meimad) that channelled $189 million to 86 small companies in a single year. These are the working reform models Europe can adopt.

Q: What is the relevance of this debate to AI and dual-use technology?

A: Defence procurement is the cleanest test case for whether Europe can act as a single technology market. The procurement-architecture problems that constrain defence startups — fragmentation, slow cycles, incumbency bias — are the same problems facing AI, quantum, and dual-use founders, expressed in a different vocabulary. Solving them in defence creates the procurement template for the rest of the European deep-tech stack.